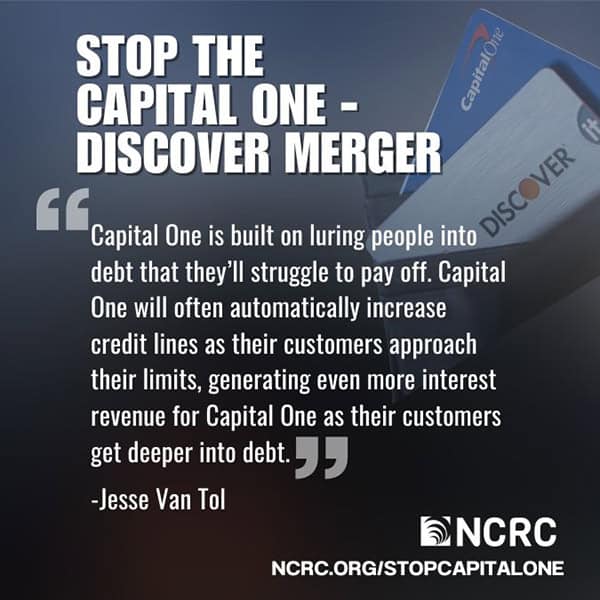

The reality behind Capital One’s shiny marketing is ugly: They carefully identify vulnerable people who are likely to get trapped in debt, then offer them credit cards to harvest interest payments on balances that the cardholders are less likely to fully pay off.

Capital One hunts for their profits in the same streets and neighborhoods where NCRC members work to reverse the wealth-denying consequences of decades of discrimination and disinvestment.

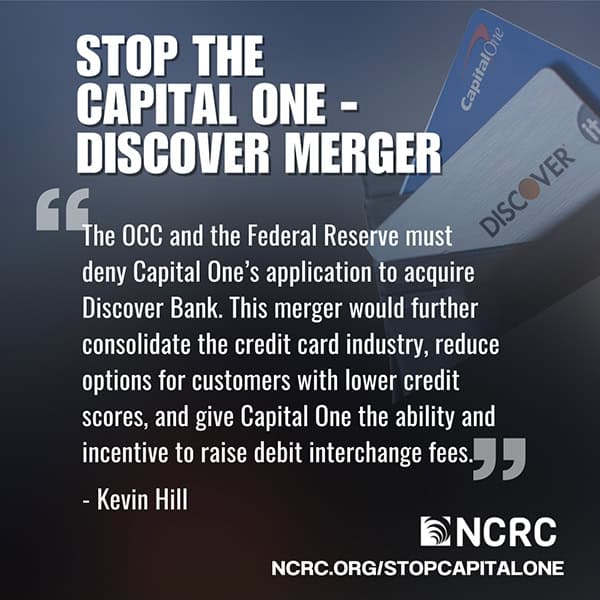

The Capital One-Discover deal also poses serious threats to competitive markets, increases systemic risk across the economy and rewards a bank with a long track record of broken promises and serious misconduct.

That’s why it’s crucial to block this bad merger. The arguments against the deal are simple, straightforward and numerous.