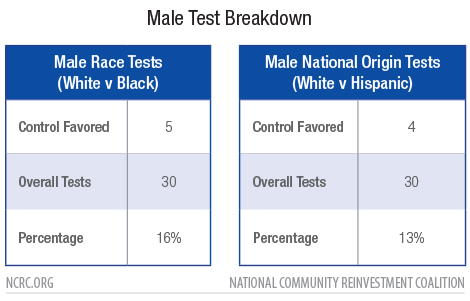

In the fair lending analysis of individual matched-pair tests for male testers, we found that five out of 30 (16%) tests revealed a difference in treatment based on race and/or national origin. Black males received worse treatment in 16% of the male tests. Hispanic males received worse treatment in 13% of the male tests.

Of the 47 different financial institutions tested in this audit, 19 (40%) institutions had at least one test that showed the control tester was favored.

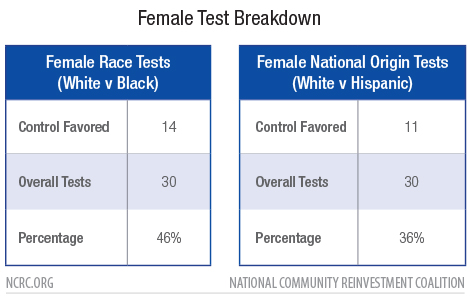

While we identified concerning behavior among the male-controlled tests, our statistical tests and fair lending review found that the female testers were more likely to be discouraged in this round of testing. We found that the Black and Hispanic female testers received worse treatment through overt statements, information asymmetry and discouragement. We found that these different types of discouragement occurred for women throughout the interaction with the loan officer. Male testers experienced this type of discouragement as well, but at a lower frequency rate. Therefore, the majority of the remainder of this paper will focus on female tester experience.

Overt statements

An overt statement of discouragement in the pre-application process occurs when the applicant who is a member of a protected class is bluntly told while information gathering only, that they will not qualify for a loan or should not apply for a loan at this financial institution or at other financial institutions. The fair lending review reveals these types of statements.

- At one financial institution, the Black Female tester was told “that my business was not the type of business they would do loans for and he stated that [X type of business] was not a stable business to be in. He spoke in a negative manner about my business saying that I would probably have some difficulty getting a loan.”

The bank officer’s statement is overt as he is outright discouraging her from not only applying for a loan at their bank but also discouraging her from inquiring about a loan at another institution by telling her that she will probably have difficulty getting a loan. The Black tester’s financial profile was stronger than the White tester, who had a business in the same industry and was informed about a business loan and given information about the application process and interest rates.

- At another financial institution, the Black Female tester was asked questions about business income and told “that if my business was not doing well, at this time I would not qualify for any type of loan.” The White tester in contrast, was never asked for her business income; instead she was recommended a line of credit and given information about interest rates and fees.

This statement is overt as the bank officer is discouraging the Black tester from applying as he has informed her that she will not qualify for a loan because she has been impacted by the pandemic. The Black tester’s financial profile was better than the White tester’s profile; furthermore, the purpose of this testing is to inquire about products due to the negative economic effects of the pandemic.

Information Asymmetry

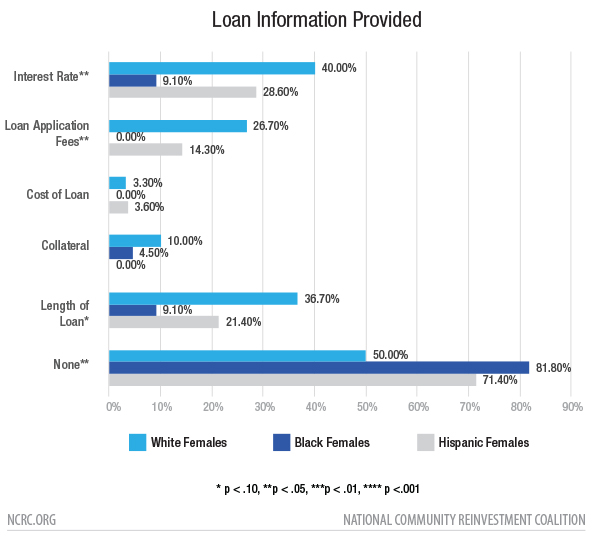

The purpose for the interaction between business owner and bank employee is the collection of information. The more information a business owner receives from the bank employee the more complete their decision making can be. Information is not limited to the number of products being offered but also to the details about these products like interest rates, fees and collateral requirements.

The offering of different products to applicants who have financially similar profiles is an ECOA violation. During the testing period, one of the lending products available was a PPP loan. The testing revealed a statistically significant difference across the banks tested with the Black female testers and Hispanic male testers provided less information about PPP loans than their White and Black counterparts. There was no significant difference between the White and Black male testers or White and Hispanic female testers in this area.

We also tested the consistency of information surrounding basic elements of a loan — the interest rate offered, loan application fees, cost of the loan, need for collateral and loan length — being provided by bank employees. There was also a “None” variable for no information provided. We found that across the marketplace a statistically significant portion of Black female testers are either not provided with any information about loan products and their features, or the information provided is limited. Asymmetric information gathering impacts the Black tester’s ability to make an educated decision compared to both the White female and the Hispanic female testers. A decision made with partial information disadvantages the borrower to such a degree that it may potentially harm the business.

Under a fair lending review at one financial institution, all three female testers spoke to the same loan officer within three days of each other about products to help their business. Each tester was told about a few products but then the loan officer steered each tester in a different direction regarding recommendations.

- The Hispanic tester was told their best option would be to contact their current bank and seek out a PPP loan.

- The Black tester was told they could receive a line of credit and was provided information about interest rates and approval times.

- The White tester was told about an Economic Injury Disaster Loan (EIDL) and how it would be “quick to get, and did not use as much scrutiny as ordinary loans.”

The offering of different products to similarly situated potential applicants is a violation of ECOA as these testers all had similar financial profiles and should have been recommended the same products, as well as provided with similar information to make a decision.

Steering to HELOC

A major problem within information asymmetry is steering an applicant to a specific product. This suggests that the loan officer is able to make the judgement for the applicant about what is best for them without giving the applicant the choice to make their own decision. Steering is a violation of ECOA. In this round of testing, five testers were offered non-business loan products, specifically a Home Equity Line of Credit (HELOC).

The fair lending review revealed that two White male testers, one Black female tester, one White female tester, and one Black male tester were offered HELOCs.

- A White male tester was told he could borrow the full amount requested by applying for a HELOC compared to applying for a regular business line of credit which would qualify for a smaller amount. The Hispanic tester was told simply they would not qualify for the full amount requested and encouraged to try a different bank.[6]

- In three different tests, the White female, Black female and Black male testers were informed that a HELOC was the only product available.

Discouragement

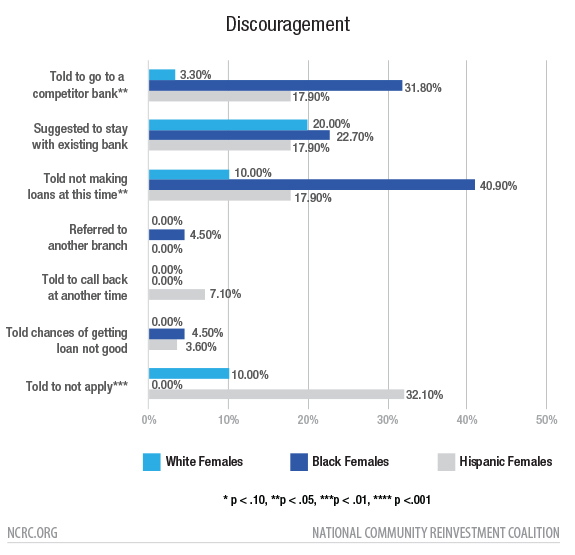

In our first PPP paper that focused on the Washington, D.C., marketplace, the fair lending review revealed that White testers were encouraged to apply for loans with thefinancial institution more often than Black testers. Encouragement to apply for a loan was revealed through statements made to different testers. In this round of testing in Los Angeles, we focused on determining if specific discouragement statements rose to the level of statistical significance. We added additional measures in the tester survey to determine if testers were being discouraged at equal levels from applying.

The collection of this new data, reveals that there are a number of mechanisms bank employees implement to discourage the Black and Hispanic female testers. Specifically, Black female testers were told to go to a competitor bank or that they were not making loans at this time. The Hispanic female testers were told not to apply. In both cases, there were statistically significant differences in treatment.

In addition to the statistical tests, the fair lending review revealed discouragement of the Black and Hispanic testers in the following ways.

- The White tester was given information about a business loan while the Black tester was “informed [that] their bank is not offering any type of business loans” and the loan officer suggested the tester go through a larger bank such as Chase, Wells Fargo or Bank of America.

This statement to the Black tester is a violation of ECOA because the tester is being discouraged from pursuing a loan at the tested financial institution as she is told that no lending is currently occurring which is not true as the White tester was told about loan products. Again, the financial profile of the Black tester was stronger than the White tester and she should not have been discouraged from pursuing a loan at the tested institution.