In late October, the federal agencies revised the Community Reinvestment Act (CRA) regulation in the most foundational and fundamental update since 1995. Banking has changed dramatically in those 28 years. For those of us in the workforce in 1995, you may recall getting your first email, likely on a computer the size of a microwave. Today that happens in your hip pocket – and the banking industry has consolidated itself down significantly as well. In 1995, there were 9,943 banks in the US. Now there are just over 4,100. And banks are much bigger in size today. The top six banks now have over $8 trillion in assets.

These two types of sweeping change were among the most important topics regulators sought to address in the new rules finalized last fall. This article will focus on how the reshaped banking industry is reflected in the new rules – specifically in the CRA examination process that is vital for driving reinvestment activity.

CRA exams were designed in that older era where banks were smaller and more plentiful. Thus, we need CRA exams that expect a smaller number of bigger banks to engage in more reinvestment activity. This intuitive connection is also borne out in the numbers: There is a clear pattern of CRA “grade inflation” in recent decades as modern megabanks were examined under the old and outmoded process.

The 2023 regulatory update created CRA exams that have the potential to hold banks more accountable. In order to account for virtual banking, CRA exams will for the first time cover all the home, small business, small farm lending and community development lending and investments that banks make. Regardless of whether a bank made a home or small business/farm loan through a branch or via the internet, the loan will now be included on a CRA exam.

A more expansive exam is doubtless a better one. But the agencies also needed to make them much tougher, in addition to much broader. One key test that CRA reform must pass is whether the reform made exams more rigorous so that banks will work more strenuously to redress redlining and help combat inequalities in wealth and homeownership.

Over the last several years 98% of banks have passed their exams. If the reform reduces ratings inflation and creates ratings that more accurately reflect distinctions in bank performance, banks are more likely to work harder, meaning they will offer more loans, investments, and services in low- and moderate-income (LMI) communities.

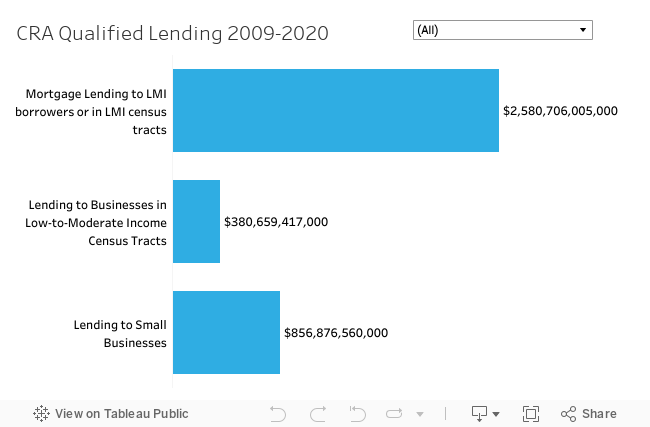

Between 2009 and 2020, banks made more than $2.58 trillion in home loans to LMI borrowers or in LMI census tracts. While this is a big number, banks can do better. Federal Reserve economists have shown that CRA increased home lending in LMI tracts by 10% to 20% under the current exams in which only 2% of banks fail. Imagine if either the failure rate increases, or the new exams reveal more distinctions in performance, so that we know how many and which banks really got a B- or C instead of just As and Bs?

If tougher grading occurs, it is possible that the next time economists conduct a CRA study, lending might increase by 20% to 30% to LMI borrowers and in LMI tracts. An increase of this magnitude is possible because studies have shown that banks, particularly larger banks, have become too conservative, reducing lending beyond what was necessary to account for the impacts of the 2008 financial crisis on creditworthiness.

New Retail Lending Test’s Promising Potential To Counter Grade Inflation

Under CRA reform, the new lending test for large banks became the most rigorous component on the new exams, creating thresholds that banks had to attain in order to achieve certain ratings. For example, if a large bank wants an Outstanding on the new lending test, they would have to make a percentage of home loans to LMI borrowers or census tracts that was 115% greater than other lenders’ percentage in a geographical area. This sort of “race to the top” incentive structure is appropriate to the “Outstanding” designation. Similarly, to pass the lending test and achieve at least a Low Satisfactory rating, the bank would need to make a percentage of loans to LMI borrowers or tracts that was 80% as much as other lenders’ percentage (there are also community benchmarks based on demographic statistics but let’s just concentrate on the market benchmarks for now). Here too the structure matches the labels: You can still just-barely pass the exam while lagging your competitors, but fall further than one-fifth behind and you lose all privileges of a passing grade. In addition to home loans, banks would have a similar evaluation for small business and small farm loans on the retail lending test.

Using historical data from 2018 through 2020, the agencies estimated that a considerably higher portion than today (more than 9%) would fail the new retail lending test unless they worked harder in the future. The great majority would pass, per the regulators’ estimations: About 90% of banks subject to the new retail lending test would pass with a Low Satisfactory or higher on the test. The agencies estimated that about 10.5% would be rated Outstanding, 47.2% rated High Satisfactory, 33.2% rated Low Satisfactory, 9% rated Needs-to-Improve, and .2% rated Substantial Noncompliance. At the same time, about one-third would be rated Low Satisfactory on retail lending, which is the equivalent of a B- or C.

The retail lending test rating is of course just one component of a bank’s “final ratings” under CRA. Large banks also have community development and retail products and services tests. These tests can also result in Low Satisfactory ratings as well as Outstanding, High Satisfactory, and the two failing ratings. Although “Low Satisfactory” is not a possible overall rating for an exam, the overall ratings would be accompanied by a range of scores for each of the component tests in the new CRA exams. Banks with Satisfactory ratings would also be assigned a final score that ranges from 8.5 to 4.5. Banks with scores closer to 4.5 are those that most likely performed in a Low Satisfactory manner on their tests, meaning that they barely passed. Since this score will now be public, banks will be subject to more accountability and are likely to work harder to make more loans and investments.

Some banks complained that the new tests were too unrealistic, creating too few opportunities to achieve Outstanding ratings and flunking too many banks. They suggested that banks would reduce their lending and other CRA activity and concentrate on fewer geographical areas to have a better chance of doing well on their exams. However, the agencies pointed out that banks should exceed the market average in order to get Outstanding ratings and that banks can perform worse than their peers and still pass with a Low Satisfactory rating. If one accepts the premise that market failure and discrimination still impede lending in underserved communities and the new CRA tests ask banks to work harder to counter these obstacles, then the new test rigor is a win-win asking the banks to stretch in a realistic fashion to make more loans and investments.

Exam Rigor Beyond The Retail Lending Test

While the retail lending test appears likely to drive down grade inflation, the agencies were not as successful in the other new tests, including the community development finance test in increasing exam rigor. They created quantitative measures, such as the dollar amount of community development finance divided by deposits, but did not create thresholds for ratings categories in the community development finance test like they did for the lending test. They point out that a lack of historical data prevented them from creating thresholds on the community development and other component tests. However, this lack of guidance on how to achieve an Outstanding grade can lead to examiner subjectivity and inconsistencies across exams, which in turn drive grade inflation. This could have been avoided by, for example, specifying that a bank cannot score Outstanding unless they have a community development ratio higher than its peers.

In addition, the qualitative measures remain under-developed and under-utilized. For example, the new retail services and products test will evaluate the responsiveness of credit and deposit products to LMI consumer needs for affordable and accessible products. The test will include a measure of the percentage of deposit accounts that are responsive, but the agencies declined to compare a bank’s percentage against its peers as part of determining a score for this part of the test. This lack of standardized comparisons again invites examiner subjectivity and ratings inflation. Moreover, the analysis of responsiveness is only included in scoring if it improves the bank’s rating – which dulls this provision’s fangs by explicitly notifying banks they will not be punished for performing badly on this test. This risks being perceived as a permissions slip for banks to fail to provide affordable products and offer a plethora of higher-cost products to LMI consumers. Traditionally underserved populations and neighborhoods already experience an over-abundance of payday and other high-cost alternatives to traditional bank products. The agencies missed an opportunity to encourage increased bank competition on affordable products in LMI communities.

The agencies anticipate developing examiner guidance and other documents for implementing the CRA regulation. Until the final regulation becomes effective in 2026, the agencies must reach out to community-based organizations and solicit their thoughts for the guidance documents.

Ideally, the agencies would hold public comment periods so people with the most at stake can have input on these draft documents. No matter how good a CRA regulation is, it will not realize its potential unless implemented rigorously. Input now from all stakeholders will promote rigor in implementation, counter ratings inflation and ultimately increase reinvestment.

Josh Silver is a Senior Fellow at NCRC.