December 20, 2021

Illinois Department of Financial and Professional Regulation

Attn: Craig Cellini

320 West Washington, 3rd Floor

Springfield, IL 62786

Comments on Advanced Notice of Proposed Rulemaking (ANPR) regarding Illinois Community Reinvestment Act

(Public Act 101-657, codified at 205 ILCS 735)

Dear Mr. Cellini:

The National Community Reinvestment Coalition (NCRC), an association of 600 community organizations dedicated to increasing access to credit for underserved communities, appreciates this opportunity to comment on the ANPR regarding the Illinois Community Reinvestment Act (ILCRA). NCRC applauds the elected officials, community-based organizations and other stakeholders who made the ILCRA possible.

Illinois joins a handful of other states that have implemented CRA laws that not only cover banks but also non-bank institutions that the federal CRA does not cover. States such as Illinois therefore are the laboratories of democracy and illustrate to the rest of the nation how to require a wide swath of financial institutions to serve all communities, but especially communities of color that were redlined and discriminated against for decades.

By increasing access to lending, investments and services, CRA laws will reduce the racial and income inequalities in our country, including unequal access to credit and wealth. The economy as a whole will benefit if these inequalities are substantially reduced and residents of undeserved and redlined communities are able to more fully participate in our economy, and improve their abilities to build wealth and provide for their families.

In this comment, we encourage the Illinois Department of Financial Regulations to:

- Coordinate developing CRA regulations with the federal bank agencies as they update their CRA regulations.

- Develop assessment area procedures that rigorously examine lending conducted through traditional bank branches and via non-branch means.

- Explicitly examine financial institutions’ performance in serving people of color and communities of color.

- Examine lending but also community development and services.

- Carefully develop a ratings system that accurately captures distinctions in performance.

- Provide the most exam weight to lending but also significant weight to community development and services.

- Develop frequent and comprehensive exams. Instead of stretching out exam cycles, use fee assessment as a way to encourage better performance.

- Develop robust public participation requirements in CRA exams and applications.

- Use CRA as a significant factor in application approvals, denials and conditional approvals; encourage the development of Community Benefit Agreements.

The Illinois Department of Financial Regulation should coordinate with the Federal agencies

One of the first questions the ANPR asks is how the Illinois Department of Financial and Professional Regulation (the Department) should coordinate with federal banking agencies as they undertake reforming federal CRA regulations in the next year. NCRC encourages the Department to work closely with the federal banking agencies during the review of federal CRA regulations. Just like Massachusetts, the Department anticipates that its examiners will jointly conduct CRA evaluations with federal examiners for banks charted by Illinois. Thus, the federal and state overall CRA evaluation and subtests should be as similar as possible. We hope that the federal agencies and the Department can jointly develop innovative improvements to the current federal CRA exams that bolster the rigor and objectively of the exams, resulting in more loans, investments and services for low- and moderate-income (LMI) and other underserved communities.

Online lenders should be covered regardless of the physical location of their offices

The ANPR asks whether the ILCRA’s scope should “include any location that offers products and services to residents of this State, regardless of the physical location.”[1] The ANPR stated that “Many other covered financial institutions offer and provide products and services electronically, via mobile and other digital channels, to Illinois residents from locations outside the state.”[2] The Department must include these online providers regardless of whether their physical offices are located in the State. Any institution licensed to make loans in the State and that make substantial numbers of loans, regardless of their delivery system, must be covered by the ILCRA.

Massachusetts’ CRA law and regulation provides a model of how to cover mortgage companies that have a variety of delivery models including online delivery. The Massachusetts’ CRA regulation applies a retail lending test and service test to them that is feasible and has likely increased lending and community development financing to undeserved communities as found in a recent NCRC white paper.[3] If these lenders are not covered, inequalities are likely to worsen because the financial industry will not be covered uniformly by a CRA law and regulation. Those institutions that are not covered would probably not make as many loans, community development financing and services in LMI and underserved communities. A Federal Reserve-sponsored study revealed that lending decreased when CRA coverage of LMI tracts was diminished.[4] From the start of a new law and regulation, therefore, it is imperative that coverage be widespread in order to achieve the statutory purposes of ILCRA.

Assessment areas should cover the State but also localities within the State

The Department should examine online lenders on a statewide basis but also develop additional assessment areas that assess the performance of these lenders in meeting the diverse needs of metropolitan areas and rural counties. The ILCRA statute states under Section 35-10(a) “each covered financial institution that provides all or a majority of its products and services via mobile and other digital channels shall have a continuing and affirmative obligation to help meet the financial services needs of deposit-based assessment areas, including areas contiguous thereto, low-income and moderate-income neighborhoods, and areas where there is a lack of access to safe and affordable banking and lending services.”[5] This provision allows for not only a statewide evaluation but evaluations at lower levels of geography.

The Massachusetts CRA examines mortgage companies at a statewide level. The only assessment area is the state.[6] This ensures that the exam will evaluate all of a mortgage company’s loans in the state, which is vital to achieving accountability on the part of the mortgage company to serve LMI and underserved borrowers. However, within a state, credit and community development needs vary across large metropolitan areas, smaller cities and rural counties.

NCRC encourages the Department to examine activity at a statewide level but also to create additional assessment areas that scrutinize activity across a diversity of urban and rural communities. The additional assessment areas should cover a significant amount of activity. The areas should include geographical areas in which the lender has a major market presence (as measured by a market share metric) but also areas that are underserved by traditional lenders. The ILCRA law requires lenders to serve undeserved areas by stipulating “…and areas where there is a lack of access to safe and affordable banking and lending services.”[7]

NCRC has developed a methodology that identifies underserved areas by considering loans per capita for all lenders in the aggregate and for online lenders. In many instances as described in a recent white paper, NCRC revealed that when all lenders were not serving an area well on the metric of loans per capita, the online lender was more successful.[8] This approach therefore seemed to identify underserved metropolitan areas (and possibly rural counties) where a CRA exam should direct online lender attention to serving LMI and underserved communities within the area.

In order to help decide how many assessment areas should be on a typical exam, the Department should consider its resources and the needs of diverse communities across the state. The Department should also conduct research and determine the spatial geographical patterns of lending of the online lenders operating in Illinois. At the very least, the Department would want choose one large metropolitan area, a smaller city and one or more contiguous groups of rural counties to assess the extent to which online lenders with significant lending volumes in each of these areas are serving needs in them.

The Department also should decide upon a target percentage of loans that the additional areas would cover – at least one third to make the exercise meaningful but hopefully half or more. In order to elevate the importance of relatively underserved assessment areas, the Department should consider weighing all the assessment areas the same. As required by the ILCRA, the Department should consult the public at large regarding the creation of assessment areas and other aspects of CRA evaluation and performance of financial institutions.

Assessment area procedures developed for online lenders and mortgage companies can also be adapted for banks and credit unions. If a bank or credit union is conducting a significant amount of lending activity outside of its branch network, the Department should consider the following assessment areas:

- The state as a whole

- Metropolitan areas and rural counties with branches

- Metropolitan areas and rural counties without branches but where a significant amount of lending activity occurs.

The Department should consider explicitly including race in CRA exams

Since redlining disproportionately victimized communities of color, the Department should carefully consider how to incorporate race into CRA exams. In our paper on mortgage companies, NCRC found that fair lending reviews accompanying CRA exams mostly consisted of descriptive statistical analysis comparing the percent of applications submitted by people of color to the percent of the population that was people of color and the percent of applications submitted by people of color to all lenders in the state. Unfortunately, our paper found that the ratings did not vary with performance of the mortgage company on the fair lending review.[9]

In a recent white paper co-authored with the Relman law firm, NCRC suggested that performance measures examining lending by race like those in the Massachusetts CRA exams could contribute to CRA ratings under a variety of approaches that would pass the strict scrutiny standard and would be found constitutional.[10] The paper recommended that on an interagency basis, the federal bank agencies could conduct periodic statistical studies and identify metropolitan areas and rural counties that either experience ongoing discrimination or exhibit significant racial disparities in access to credit. If the federal agencies adopt this recommendation, the Department could collaborate on this study, which could identify areas in Illinois that CRA exams could target for addressing racial disparities.

In these areas, fair lending performance measures could contribute to CRA ratings. The performance measures could receive a separate rating or score and thereby contribute to the rating for the subtests and for the overall rating. Alternatively, the performance on the racial and ethnic measures could boost a rating if the performance is commendable. We would prefer the first alternative but offer the second in the interests of presenting various options for assuring success against a strict scrutiny standard. Of course, as occurs currently in federal CRA evaluations, if a fair lending review uncovers discrimination, the Department should lower a bank’s rating, particularly if the discrimination is not confined to a rogue employee or office but is widespread across the institution.

In addition to performance measures for people of color, NCRC suggests that the Department consider developing a category of underserved tracts. The subtests of the CRA exam would then examine lending, service, and community development activities in these tracts just as the exams now do for LMI tracts. In a previous report, NCRC describes that underserved tracts would be identified via a metric of loans per capita (using households as the denominator in home lending and small businesses as the denominator for small business lending).[11] Tracts in the lowest quintile of loans per capita would be designated as underserved. NCRC found that across the nation, 57% of underserved tract residents, on average, were people of color in these tracts. Therefore, using underserved tracts on CRA exams would be another way to increase the focus on communities of color.

The NCRC and Relman white paper identify several other methods for increasing the attention of CRA exams on people and communities of color. For example, CRA regulations should mandate that assessment areas cannot arbitrarily exclude communities of color just like assessment areas currently cannot exclude LMI tracts. In addition, on the criteria of innovation and flexibility on the subtests, CRA exams should consider innovative Special Purpose Credit Programs that target formerly redlined communities.[12] Finally, CRA exam performance context analysis should identify communities of color in the assessment areas that are underserved and whose needs should be addressed by institutions in the area.

Exam subtests should include community development in addition to lending

One area of coordination the Department should engage in with the federal bank agencies is exam structure. The Federal Reserve’s ANPR outlined an intriguing exam structure of a retail lending test, a retail service test, a community development (CD) finance test and a CD service test.[13] The retail lending test would resemble the current test with the exception that community development lending would be moved to the CD finance test.

The retail services test would serve the important functions of not only assuring that underserved communities are served by branches but that online delivery of bank services is actually reaching people of color and LMI customers. The retail service test would assess the number and percent of deposit products for LMI borrowers and/or LMI and other underserved tracts. The Department should work with the federal agencies in the development of improved data, performance metrics and CRA exam tables to better assess retail services delivery.

The CD finance test would examine CD lending and investing. Lastly, the CD service test would scrutinize the provision of CD services such as homebuyer counseling, financial education and technical assistance for small businesses.

The Federal Reserve framework seems well suited not only for banks but also mortgage companies and credit unions. The retail lending test would be a major test for these lenders. In the area of community development, mortgage companies and credit unions do not typically have as high volume of CD finance as banks; they will not usually engage in Low Income Housing Tax Credit (LIHTC) or other complicated CD financing. Hence, combining CD lending and investing makes sense since overall levels of financing will be lower for these nonbanks.

However, they will engage in CD finance such as donations that further community development so a CD finance test should ensure a sufficient level of CD finance. For example, the Massachusetts’ Division of Banks CRA exam of the Harvard University Employees Credit Union documented about $100,000 in grants for social service providers including food banks and organizations that provide social services to the homeless and at-risk families.[14] Likewise, the Liberty Bay Credit Union offered about $87,000 in grants to similar organizations.[15]

As these examples show, the Massachusetts exams often describe grants and other support for community-based organizations. This activity must be encouraged by a CD finance test because it is supporting an infrastructure of counseling agencies and other community organizations that assist underserved LMI and people of color enter the financial mainstream and acquire access to loans and banking products. Lastly, a separate CD service subtest would assess the extent to which the lenders engage themselves in CD services such as counseling that directly benefit underserved populations or technical assistance to community-based organizations that assist underserved populations. The Liberty Bay Credit Union, for instance, created curriculum for financial education that it delivered in conjunction with community-based organizations and in its branches.[16]

Ratings must reflect distinctions in performance

The ILCRA law (Section 35-15c) mandates that financial institutions are to receive one of four ratings: Outstanding, Satisfactory, Needs to Improve and Substantial Noncompliance.[17] We encourage the Department to augment the four ratings in order to create CRA evaluations that more accurately reflect distinctions in performance.

The shortcoming of four ratings in federal CRA exams is that they do not reveal distinctions of performance to the extent desired by either banks or community organizations. Banks seek to differentiate themselves from their peers. However, that objective is frustrated since about 98% pass and 90% receive a Satisfactory rating on federal exams.[18] Community organizations seek to push lenders with lower ratings to improve their performance, but this is challenging when CRA exams make it difficult to determine which lenders might be barely passing and performing in a manner below the Satisfactory rating they received on their exam. Five ratings are more successful in revealing distinctions in performance but only to the extent that the regulatory agency actually uses the five ratings.

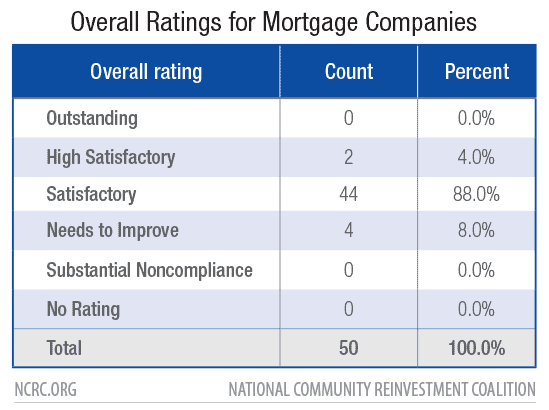

The above chart shows that Massachusetts CRA has five overall ratings. Of the 50 exams in NCRC’s sample in our white paper, 88% of mortgage companies received a Satisfactory rating, 4% received a High Satisfactory rating, and 4% received a Needs to Improve rating. The Division of Banks did not award a single one an Outstanding or Substantial Noncompliance rating.[19]

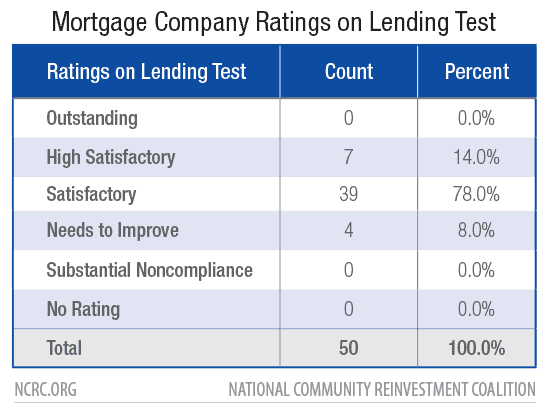

The lending test chart below shows that five ratings have potential to reveal more distinctions in performance. In this case, eleven lenders received either High Satisfactory or Needs to Improve. Still none received Outstanding or Substantial Noncompliance. While an improvement over the distribution of overall ratings, the ratings were still compressed and could have been more successful in revealing distinctions in performance.

The Federal Reserve Board (Board) in their Advance Notice of Proposed Rulemaking (ANPR) proposed performance ranges for quantitative measures to assign CRA ratings to various levels of performance.[20] For example, as discussed in NCRC’s white paper, the average percent of mortgage company loans to LMI borrowers was higher for companies receiving High Satisfactory as opposed to Satisfactory ratings on the lending test.[21] Ranges could be assigned to different ratings; the ranges would capture the extent to which a particular company exceeded or fell below the industry or demographic benchmarks. For example, on the industry (aggregate lender) benchmark for percent of loans in moderate-income tracts, the range for Outstanding could be 150% and higher above the industry benchmark. The ranges could be developed based on an analysis of performance over a number of years, using data from CRA exams in a manner similar to the NCRC analysis.

If the Department opts against five ratings, it can develop a point scale corresponding to the four ratings. When a lender scores in the lower part of a range of a point scale for a rating such as Satisfactory, the public would know that the performance is actually more akin to a Low Satisfactory rating (or Satisfactory as opposed in High Satisfactory in Massachusetts’ ratings system).

Exam weights should emphasize lending but also provide sufficient consideration for services and community development

Over the decades, federal CRA exams have provided the most weight to the lending test. Massachusetts generally follows this approach. At the federal level, the large bank exam provides 50% weight for the lending test with 25% each for services and investment tests. Massachusetts likewise has this weighting scheme for all banks. In addition, Massachusetts has a similar emphasis on the lending test for credit unions.[22]

Providing the most weight for the lending test is consistent with the need to eliminate redlining. Private sector financial institutions would refuse to make loans in neighborhoods they redlined, even when they had branches in those neighborhoods. As a result, neighborhoods could not develop a robust number of homeowners and small business owners, and would decline economically.

While providing the most weight for a lending test, the Department should carefully develop weights for services and community development after deciding upon a test structure. Services including branches and deposit accounts are critically important as an affordable alternative to payday lenders, check cashers and other fringe outlets that offer high-cost products. Services also help customers establish relationships with their financial institutions and build their credit, which is vital to qualifying for loans.

Like services, community development activities are needed for successful and economically viable neighborhoods. A neighborhood cannot thrive if contains homeowners but a dearth of small businesses, commercial corridors, green space and recreational facilities. Community development financing supports the development of neighborhood institutions and infrastructure. Finally, community development services including counseling and technical assistance help establish a customer base in undeserved neighborhoods that can access the financial mainstream. In sum, the variety of activities on CRA exams are important and must receive sufficient consideration.

Exams must be frequent and broad in scope to be effective

The Department must opt for frequent exams. Exams should not occur less often than once every two or three years. Incentives to perform well diminish significantly if a lender is examined once every four or five years as permitted in some circumstances by the Massachusetts regulations and examination practice.[23] A lender will have more incentive to manipulate the exam cycle when the cycle is stretched out. For example, it can perform poorly over a longer period of time (three to four years) and ramp up activity in the last year before an exam. The result is fewer loans, investments and services for LMI neighborhoods and communities of color.

Even lenders that received an Outstanding rating on its last exam should not receive a stretch out. A more effective incentive from the perspective of communities in need of access to credit and capital is lower exam fees for good performers and higher ones for poor performers as contemplated by the Department.[24] Low scoring banks would be motivated by increased expenses to perform better on the next exam. Communities would not experience fewer loans, CD financing and services resulting from any slackening of effort by groups of lenders experiencing an exam stretch out and would benefit from more reinvestment from those seeking to lower their fees.

As well as being regular, exams should be broad in scope instead of narrow or complaint-driven. Complaints from a community are important and must be considered by examiners. However, they should not guide exam schedules because members of the public do not have the resources or expertise to effectively monitor the wide variety of lenders serving the state. Only the Department has the resources for regular monitoring and examination.

CRA as a factor for mergers, branch openings and license renewals

We are pleased that the ILCRA in Section 35.10 requires the Department to consider the CRA record of lending institutions when they seek to renew their licenses, merge or establish branches. These applications must be accompanied by a 60-day public comment period[25] so members of the public can comment on whether the lending institution is meeting community needs and should have its application approved, approved with conditions to improve CRA or fair lending performance, or denied.

The Department must establish clear and easy methods for informing the public when lenders submit these applications. In addition to notices on its website, the Department should establish an email/mail list of interested stakeholders and should also proactively provide notices on social media. It should ensure that traditionally underserved communities, particularly communities of color and low- and moderate-income communities, have access to notices of comment periods of upcoming CRA exams and applications.

If a lending institution has failed its CRA exam, it must not be allowed to submit an application until it passes an exam. If a lending institution has a poor record of CRA and fair lending performance and has clear deficiencies as indicated in its most recent CRA exam or publicly available data, the Department must highly scrutinize its application and consider approvals conditional on improved performance. The Department should encourage the institution to develop a plan for improvement often referred to as a community benefits agreement[26] that is developed in conjunction with community organizations, including those that are operated by people of color and serve communities of color.

An application approval must be regarded as a privilege, not a right. It is a critical time for CRA and fair lending enforcement during which the Department and the public ensures that the lender is abiding by its CRA and fair lending responsibilities to serve communities in a fair and equitable manner.

Conclusion

NCRC appreciates the opportunity to comment on the ANPR for the ILCRA. The Department has an opportunity to develop innovative and rigorous CRA exams based on the experience of federal and state agencies in implementing CRA. Comprehensive exams with well-developed assessment areas, that have performance measures for people of color and communities of color, have five ratings, that contribute to the Department’s consideration of applications, and that have ample opportunities for public input have the potential to significantly increase access to capital and credit for undeserved communities in Illinois.

Thank you kindly for consideration of our views in this important matter. If you have any questions, please contact Josh Silver, Senior Advisor at jsilver@ncrc.org or myself at jvantol@ncrc.org.

Sincerely,

Jesse Van Tol

President and CEO

[1] Illinois Department of Financial and Professional Regulation Illinois Community Reinvestment Act: Advance Notice of Proposed Rulemaking, p. 2, August 31, 2021, https://www.idfpr.com/News/2021/2021%2007%2020%20IL%20CRA%20Advance%20Notice%20of%20Proposed%20Rulemaking%20Outline.pdf

[2] Ibid.

[3] Josh Silver, NCRC, Massachusetts CRA For Mortgage Companies: A Good Starting Point For Federal Policy, July 2021, https://ncrc.org/massachusetts-cra-for-mortgage-companies-a-good-starting-point-for-federal-policy/

[4] Lei Ding and Leonard Nakamura, Don’t Know What You Got Until It’s Gone’ — The Community Reinvestment Act in a Changing Financial Landscape., Working paper (Federal Reserve Bank of Philadelphia). Philadelphia, Pennsylvania: Federal Reserve Bank of Philadelphia, February 2020. https://doi.org/10.21799/frbp.wp.2020.08.

[5] ILCRA, Section 35-10 (a)

[6] Silver, Massachusetts CRA For Mortgage Companies, op.cit.

[7] ILCRA, Section 35-10 (a)

[8] Josh Silver, How Can Geographical Areas On CRA Exams Work For Branchless Banks?, NCRC, January 2021, https://www.ncrc.org/how-can-geographical-areas-on-cra-exams-work-for-branchless-banks/

[9] Josh Silver, NCRC, Massachusetts CRA For Mortgage Companies, op. cit.

[10] Brad Blower, General Counsel, NCRC; Josh Silver, Senior Policy Advisory, NCRC; Jason Richardson, Director of Research and Evaluation, NCRC; Glenn Schlactus, Partner, Relman Colfax PLLC; Sacha Markano-Stark, Attorney, Relman Colfax PLLC, Adding Robust Consideration Of Race To Community Reinvestment Act Regulations: An Essential And Constitutional Proposal, NCRC, September 2021, https://ncrc.org/adding-robust-consideration-of-race-to-community-reinvestment-act-regulations-an-essential-and-constitutional-proposal/

[11] Bruce Mitchell, PhD. and Josh Silver, Adding Underserved Census Tracts As Criterion On CRA Exams, NCRC, January 2020, https://ncrc.org/adding-underserved-census-tracts-as-criterion-on-cra-exams/

[12] For a recent Department of Housing and Urban Development Memorandum on these programs, see https://www.hud.gov/sites/dfiles/FHEO/documents/FHEO_Statement_on_Fair_Housing_and_Special_Purpose_Programs_FINAL.pdf

[13] Federal Reserve Board issues Advance Notice of Proposed Rulemaking on an approach to modernize regulations that implement the Community Reinvestment Act, September 21, 2020, https://www.federalreserve.gov/newsevents/pressreleases/bcreg20200921a.htm

[14] August 2020, CRA Exam of Harvard University Employees Credit Union, Commonwealth of Massachusetts, Division of Banks, pp. 7-8, https://www.mass.gov/doc/harvard-employees-credit-union-public-evaluation/download

[15] December 2019 CRA exam of Liberty Bay Credit Union, p. 15, https://www.mass.gov/doc/liberty-bay-cu-cra-pe/download

[16] Liberty CRA exam, p. 15.

[17] ILCRA Section 35-15c

[18] Josh Silver and Jason Richardson, Do CRA Ratings Reflect Differences In Performance: An Examination Using Federal Reserve Data, NCRC, May 2020, https://ncrc.org/do-cra-ratings-reflect-differences-in-performance-an-examination-using-federal-reserve-data/

[19] Josh Silver, NCRC, Massachusetts CRA For Mortgage Companies, op. cit.

[20] Federal Reserve ANPR, op. cit.

[21] Josh Silver, NCRC, Massachusetts CRA For Mortgage Companies, op. cit.

[22] Massachusetts Division of Banks, Component Test Ratings, https://www.mass.gov/regulatory-bulletin/23-102-cra-ratings-policy

[23] Massachusetts Division of Banks, Alternative CRA Examination Procedures, https://www.mass.gov/regulatory-bulletin/13-105-alternative-cra-examination-procedures

[24] Illinois Department of Financial and Professional Regulation Illinois Community Reinvestment Act: Advance Notice of Proposed Rulemaking, p. 3.

[25] Federal regulations establish a 30 day comment period for applications but this time period is often insufficient for communities to learn about the applications in time to prepare comments.

[26] For an example of community benefits agreements, see https://www.ncrc.org/ncrc-and-mt-bank-announce-43-billion-community-growth-plan-to-support-underserved-and-communities-of-color-small-businesses/