Nearly $3 trillion in home and small business loans from banks went to low- and moderate-income (LMI) borrowers and communities over the last decade. Proposed changes to the Community Reinvestment Act (CRA), which requires banks to make loans in all of the communities where they take deposits, including poor ones, could significantly decrease this lending, putting at risk billions in lending each year nationwide.

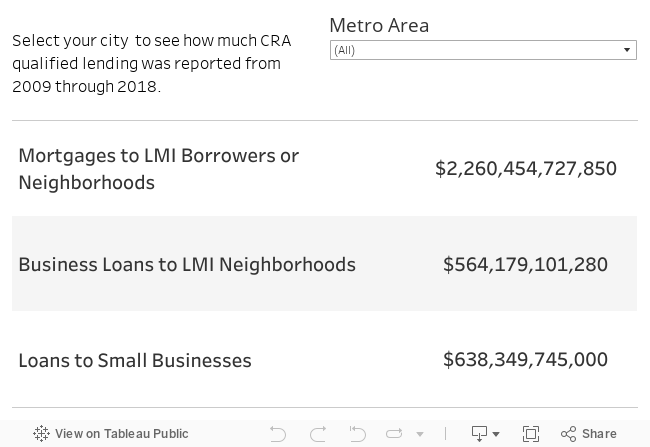

An NCRC analysis of lending data reported by banks showed banks issued more than $2.2 trillion in home loans and more than $564 billion small business loans to LMI borrowers and communities from 2009 through 2018.

The proposed changes to CRA rules, from the Office of the Comptroller of the Currency (OCC) and Federal Deposit Insurance Company (FDIC), would allow banks to fail their CRA exams in nearly half of the geographical areas in which they are examined. Common sense, supported by Federal Reserve research, suggests that lending in some communities would decrease. Banks could choose to concentrate their lending in some places and ignore others – potentially nearly half of the communities where current rules now require them to make loans. Moreover, the exams would feature a single metric (CRA activities divided by deposits) that would motivate banks to favor large deals, including sports stadiums, over small dollar home and small business lending.

See what is at risk in your community with this tool. Include these findings in a comment letter about the proposed rules. Submit your comment by March 9, 2020. Visit Treasure CRA for more details about how to comment.

Methodology

This research considered loans with low or moderate income (LMI) borrowers or in LMI census tracts to be CRA qualified. In addition, business loans to businesses that earned less than $1 million a year received CRA credit. There is an unknown degree of overlap between business loans that are both in an LMI tract and to a small business so we have kept them as separate figures for this analysis. All dollars are adjusted for inflation to January 2018 values. https://data.bls.gov/cgi-bin/cpicalc.pl .