Last week , BB&T Corporation, SunTrust Banks, Inc. and the National Community Reinvestment Coalition (NCRC) announced their $60 billion community benefits plan for the region served by Truist Financial Corporation, the combined company to be created through the proposed merger of the two banks. When this merger is complete, it will be the sixth largest bank in the country. Because it will be so big, the merger has the attention of critics who say it is too big, including some members of Congress, where the House Financial Services Committee scheduled a hearing on the deal today.

When banks merge, Community Reinvestment Act (CRA) provisions require that they show how the merger will positively impact the communities that they are chartered to serve.

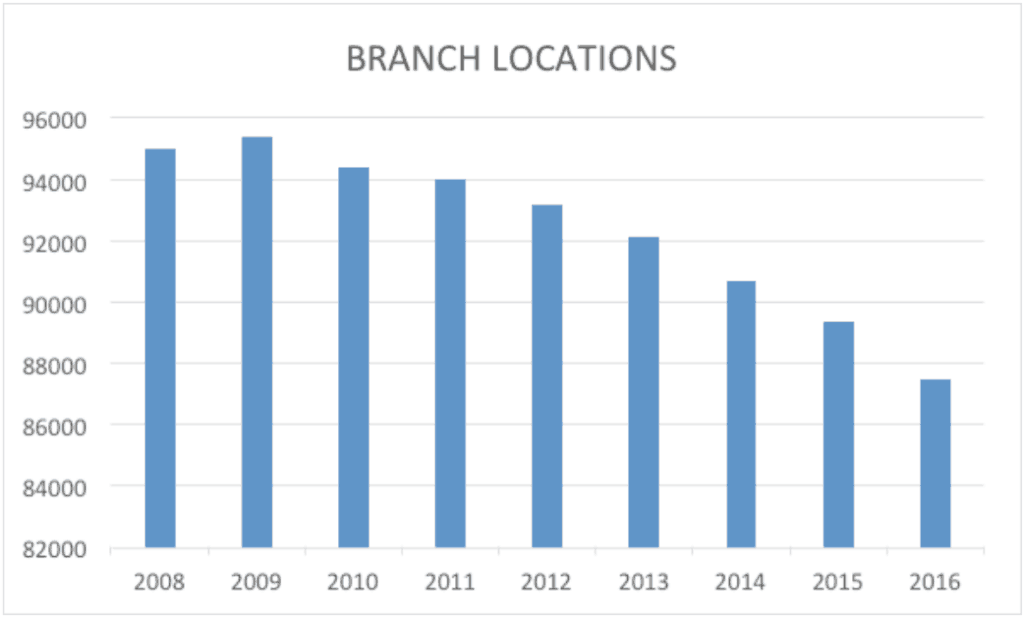

Banks often tout the benefits of merging in terms of service, citing larger networks of branches and ATMs as a benefit to the consumer. However, several studies note that these benefits come with drawbacks. Instead of providing larger networks with expanded financial services access, banks often identify the cost savings of closing branch locations as a benefit for their shareholders. In fact, the closures can result in the creation of banking deserts, especially in rural areas of America’s heartland, negatively impacting consumers in several ways.

The damage of diminished financial services access doesn’t end there. The inconvenience experienced when a local branch closes has wider repercussions in the concentration of markets and the loss of competition which reduces people’s ability to have a choice of banks.

When banks close a local branch, that community’s small business lending is often severely impacted as well. Small business lending is largely a relational process: the branch manager or small business specialist build personal connections with local businesses and through those relationships glean ‘soft information’ about the businesses, which includes details on the risks of lending to them. Several studies have found that branch closures disrupt those relationships, reducing small business lending in a community by as much as 20% for years following the closure of a single branch even when there is a network of other local banks nearby.

As branches close, especially in places that lack a large number of other banks, more and more families become unbanked. This hurts their chances to build credit and wealth, and it also makes it more likely that they will make use of alternative financial providers like payday lenders. This burdens consumers with debt they struggle to repay and further stresses low- and moderate-income (LMI) communities. The decline in the number of banks that operate in a community has also been shown to correlate with an increase in the fees that the remaining banks charge to their consumers. This increase in fees happens despite the lower operating costs incurred by the bank.

As recently as 2004, there was also a correlation between mortgage lending and bank branch locations. But recent studies have found that mortgage lending is no longer impacted when branches close. There are a few reasons for this. The 2010 Dodd-Frank Act implemented the Qualified Mortgage (QM) Rule, requiring lenders to meet several stringent underwriting requirements before they could sell the loan to Fannie Mae or Freddie Mac. These requirements were not radical. For example, lenders needed to verify that the borrower had the means to repay the debt.

But the new QM rule coincided with a larger shift within the mortgage industry from a relational business like the small business market to a technological one. As the internet and other advances became more pervasive and powerful, non-banks like Quicken Loans, PennyMac and Loan Depot became more popular with borrowers. In 2016, non-banks made half of all mortgage loans in the United States. Unlike banks, these lenders operate with less oversight since CRA doesn’t apply to them. As banks merge and close branches in the communities they serve, non-banks stand to benefit, claiming more of the mortgage market and shielding lenders from scrutiny for issues like discrimination and redlining.

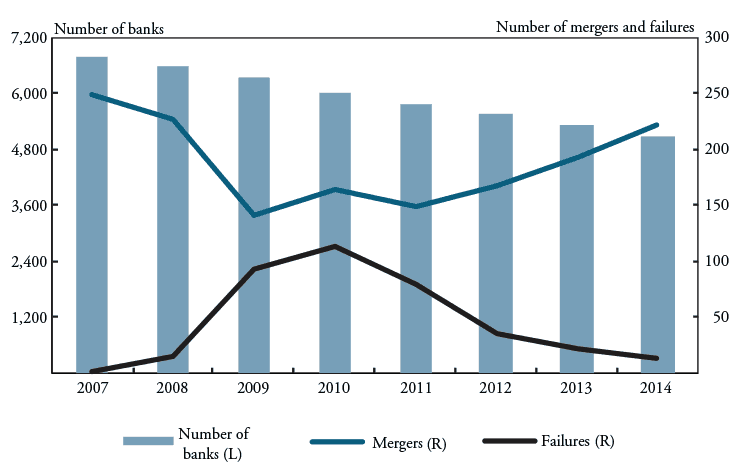

Since the 1990s, we have seen a global consolidation of banks as interstate banking and technology have allowed banks to grow into national networks with thousands of local branches and billions of dollars in assets. Following the Great Recession, the number of mergers declined somewhat, but since 2011 they have begun to rise again. Community banks in the United States have been particularly impacted, with larger banks gobbling up smaller institutions at an alarming rate. Community banks comprised 57% of deposits and 70% of bank branches in 1994. Today, they only hold 20% of deposits and account for 44% of branches.

Taken as a whole, the impact on communities when banks merge is neutral at best, and usually brings more negatives than positives. The result depends on a variety of factors, including how many other banks are left operating in the community, how healthy the local economy is and how many people live there. CRA requires that banks prove that their merger provides a public benefit – higher fees, less business lending and more unbanked families don’t meet that requirement.

The merger of BB&T and SunTrust is the largest and most recent step in the ongoing consolidation of community banking across the country. The potential for negative impacts on many communities was significant, which is why NCRC and our community organization members engaged in a series of discussions with the merging banks to create a community benefits plan. The $60 billion plan is the largest ever between banks and the communities they serve, and it will provide a much-needed influx of investment into critical programs that improve affordable housing, mortgage lending, small business development and economic development projects to LMI people and communities across most of the eastern half of the country.

Seeking a community benefits agreement with banks is a step every community can take. For information on how to get the ball rolling, contact an NCRC organizer today.

Photo by Michal Prucha via Unsplash

Jason Richardson is Director of Research and Bruce Mitchell is Senior Research Analyst at NCRC.