The release of this data is a positive step and we are encouraged by its publication. At this time, there is very little known about lending to businesses in the U.S. The Consumer Financial Protection Bureau (CFPB) is beginning to implement Section 1071 of the Dodd-Frank Act, a provision that will require lenders to report applications for loans made to businesses. These data will provide lenders, regulators and the public a much clearer understanding of which businesses have been able to access credit to expand.

In the meantime, the PPP loan data offers a unique opportunity for researchers that NCRC would like to support. To that end, NCRC will make the full geocoded data for these loans available to our members or media organizations. These data will be provided without representations or warranties. Members should contact jedlebi@ncrc.org for more information, while media organizations should contact awiltse@ncrc.org.

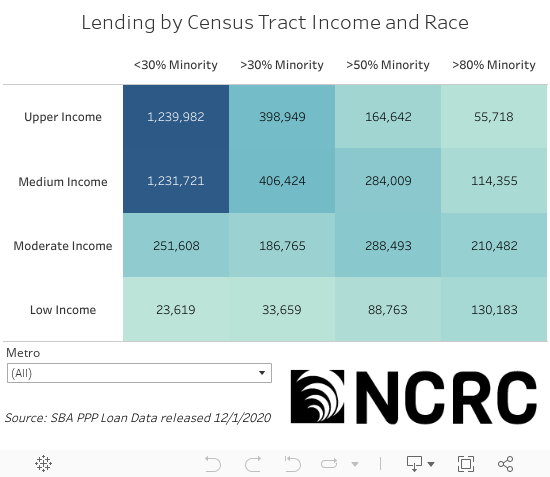

Analysis of previously released PPP data as well as stories from NCRC member organizations and our own mystery shopper testing suggested that businesses owned by people of color or located in lower-income neighborhoods and communities of color were less likely to get a PPP loan. In this preliminary analysis, a clear pattern emerged of greater investment in upper- and middle-income census tracts with a low percentage of loans in lower-income or majority minority census tracts.