Washington, DC – Today, on the anniversary of the date the Community Reinvestment Act (CRA) was signed into law by President Jimmy Carter in 1977, National Community Reinvestment Coalition (NCRC) President and CEO John Taylor made the following statement:

“The signing of the Community Reinvestment Act into law was a critically important moment for economic fairness in the United States. The affirmative obligation that banks serve and make safe and sound loans in the communities where they are chartered, including low- and moderate-income neighborhoods, has opened doors to economic opportunity for millions of working Americans.”

“Today, action should be taken to modernize the law and expand it to cover other institutions such as credit unions and independent mortgage companies, so that its benefits will be felt even more broadly.”

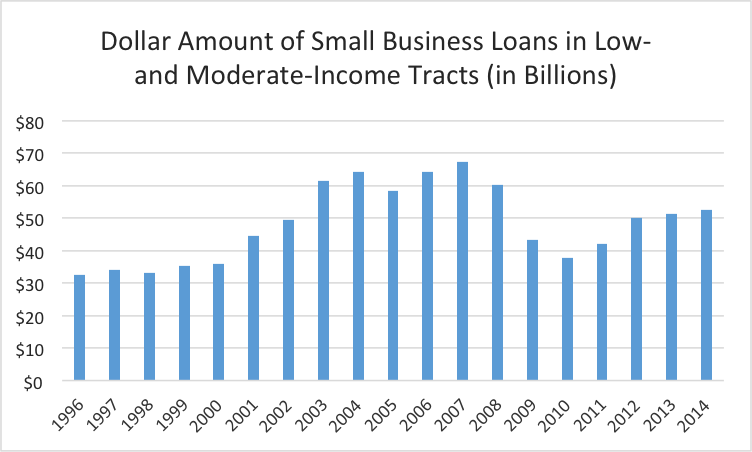

- Since 1996, CRA-covered banks issued more than 22 million small business loans in low- and moderate-income tracts, totaling more than $918 billion.

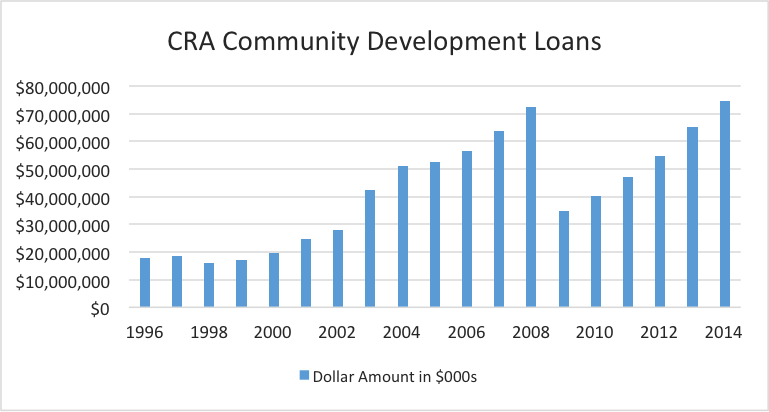

- Since 1996, CRA-covered banks made more than $796 billion of community development loans. Community development loans support affordable housing and economic development projects benefiting low- and moderate-income communities.

- The annual dollar amount of community development loans increased 321 percent from $17.7 billion in 1996 to $74.6 billion in 2014. The annual dollar amount likewise increased 85 percent from 2010 to 2014.

- Banks and their affiliated mortgage companies remain the primary lenders to low- and moderate-income borrowers buying homes. Banks and their affiliates made 311,017 home purchase loans to low- and moderate-income borrowers during 2014, in contrast to the 219,329 home purchase loans made by independent mortgage companies to these borrowers.

- CRA-covered bank home-purchase loans remain more affordable than non-CRA-covered independent mortgage company loans. About 28.1 percent of independent mortgage company home purchase loans to low- and moderate-income borrowers were high cost, as opposed to 16.8 percent for banks during 2014. Independent mortgage companies were 1.67 times more likely (28.1 percent divided by 16.8 percent) to issue a high-cost loan to a low- and moderate-income borrower than a bank.

- Economists Robert Avery and Kenneth Brevoort also find that CRA-covered lending is safer and sounder than non-CRA-covered lending. They report that when a larger share of lending was issued by CRA-covered banks than by independent mortgage companies, a neighborhood experienced lower delinquency rates and less risky lending. This study, which can be found here, is one of many affirming the safety and soundness of CRA-covered loans.

_______________________________

Chart source: NCRC calculations of data from the Federal Financial Institutions Examination Council (FFEIC) webpage, see http://www.ffiec.gov/craadweb/aggregate.aspx for data on community development lending and small business lending by year.